Stock in Focus: Alphabet (NASDAQ:GOOG/GOOGL)

CommSec

CommSec

19 August 2025

How is the world’s most famous search engine adapting to a landscape being rapidly reshaped by AI?

"Just Google it."

Only a handful of companies have become so globally prolific that over time their names become common verbs used in everyday conversation. Google is one of them.

Alphabet (NASDAQ: GOOGL (Class A) / GOOG (Class C) is a holding company that wholly owns internet behemoth Google. (Note: Class A GOOGL shares come with one vote per share, while Class C GOOG shares have no voting rights.)1 Founded in 2015, 17 years after Google itself was founded, the Mountain View, California-headquartered holding company derives slightly less than 90% of its revenue from Google services, the vast majority of which is advertising sales.2

Alongside online ads, Google Services houses sales stemming from Google's subscription services (YouTube TV and YouTube Music among others), platforms (sales and in-app purchases on Play Store), and devices (Chromebooks, Pixel smartphones, and smart home products such as Chromecast).3

Google's cloud computing platform, or GCP, accounts for roughly 10% of Alphabet's revenue, with the firm's investments in up-and-coming technologies such as self-driving cars (Waymo), health (Verily), and internet access (Google Fiber) making up the rest.4

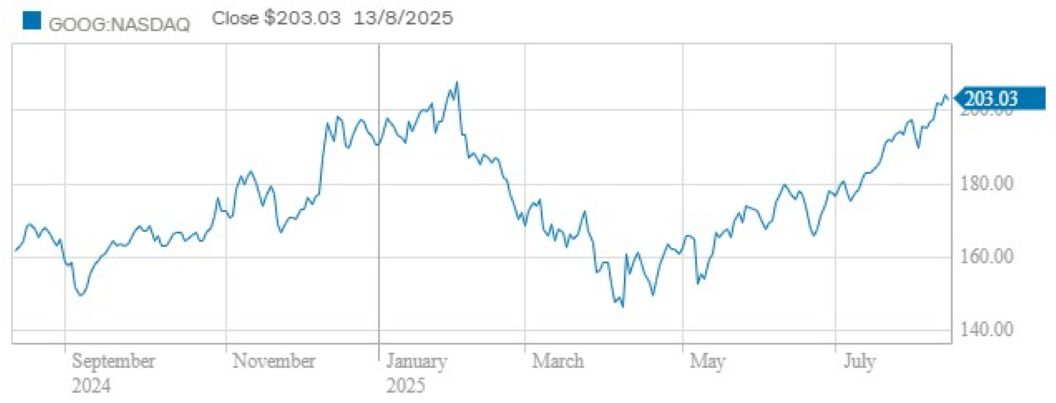

Alphabet (GOOG) hit a share price record of US$205.89 on 4 February 2025. It fell to below US$150 in April but has been on a steady incline since, closing at just over US$203 on 13 August 2025. Morningstar maintains a fair value stock estimate of US$237 for Alphabet,5 suggesting any price below this is ripe to jump in and buy.

Source: NASDAQ/CommSec, as of 14/8/25.

Letters & numbers

On 23 July 2025, Alphabet announced some rather eye-watering Q2 2025 financial results, including a 13% year-on-year increase in consolidated revenues to US$96.4bn. Google Cloud saw the biggest relative increase in revenues among Alphabet’s subsidiaries, jumping 32% to US$13.6bn and driven by growth in core GCP products, AI infrastructure and generative AI solutions.6

Alphabet and Google CEO, Sundar Pichai, said:

“We are leading at the frontier of AI and shipping at an incredible pace. AI is positively impacting every part of the business, driving strong momentum… and our new features, like AI Overviews and AI Mode, are performing well.”7

Yet despite its eager march to AI development and monetisation, Alphabet is not leaving behind what made it famous and profitable to start: search.

"Google Search's 12% year-over-year growth, accelerating from 10% growth last quarter, further reflects Google Search's resilience in the face of both gen AI-infused competitors as well as a tough macro, with spending on Search coming in well ahead of our prior 8% growth estimate," highlights Morningstar.8

Since 2009, Google Search has controlled more than 80% of the general search market – 90+% when looking only at mobile devices.9 Morningstar “[sees Alphabet’s] investments in AI as a continuation of this effort to safeguard its core product, Google Search.

"We believe that by leveraging generative AI, Google can not only improve its own search quality via features such as AI overviews, but also improve its advertising business by augmenting its ability to target customers with relevant ads.”10

Buy or sell?

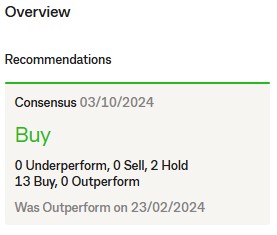

As of 14 August 2025, there is a strong “buy” consensus for Alphabet stock.

Source: CommSec.

Morningstar is unequivocal when explaining why it believes Alphabet’s current stock price is noticeably below its fair value estimate.

“We view Alphabet as a conglomerate of stellar businesses,” Morningstar noted in its July Equity Analyst Report.

“With solutions ranging from advertising to cloud computing and self-driving cars, Alphabet has built itself into a true technology behemoth, generating tens of billions of dollars in free cash flow annually.”11

Morningstar is also confident that “Alphabet has a huge opportunity in the lucrative public cloud space as a key cloud vendor to enterprises looking to digitize their workloads”.12

It argues the company’s “core advertising business is deeply entrenched in advertising budgets, allowing [it] to benefit from a secular increase in digital advertising spending [and] reinvest in growth areas such as GCP, AI-infused search, and aspirational projects such as Waymo”.13

On the bearish side, however, Morningstar warns that “regulators around the world are keying in on Alphabet’s search dominance and could upend the search market through the imposition of deep, structural changes in the search space”.14